As you may recall, the Spectator reported some weeks ago on the local implications of the scandal rocking Toronto-based private debt firm Bridging Finance Inc (BFI); namely, that Membertou First Nation borrowed $6.8 million from Bridging to finance its purchase of a stake in Novaporte, Albert Barbusci’s imaginary Sydney harbor container terminal.

Recent CBC coverage added some new information to this initial story — specifically, the size of Membertou’s stake (12.5%) and the size of Bridging’s stake (2.5%) — but it also characterized BFI as a “venture capital” firm, which I don’t think is correct.

Natasha and David Sharpe, 11 April 2019 (Source: Bridging Finance Inc)

Bridging Finance, which was placed in receivership on April 30 at the behest of the Ontario Securities Commission (OSC), is a private debt firm. Its business model, as described by the receiver, Pricewaterhousecoopers (PwC), in its initial report, is to “raise capital from investors for the purpose of making loans to corporate borrowers.” An article about the company in the Globe and Mail’s Report on Business said the firm specializes in “alternative financing” or “bridge loans” to “middle-market companies considered too risky for traditional bank financing. ” It does this through a grab-bag of funds in which investors — retail and institutional — buy “units.” It makes money the way “alternative lenders” do — via high interest charges and fees.

That’s a very different animal from venture capital, which generally involves an investor putting money into an early-stage company in return for an ownership stake and a say in decision-making. The venture capitalist makes money if they can sell their shares — either back to the company’s owner or via an initial public offering (IPO) — for more than they initially paid.

Private debt companies can and do take ownership stakes in firms — as noted, Bridging has taken what Barbusci describes as a “minimal” stake in Novaporte — but it’s not their bread and butter.

Value

I’ve chosen to illustrate this section with a picture of Warren Zevon because I like him more than I like Warren Buffet.

The other reference that struck me as requiring a more nuanced consideration was the “value” of Novaporte. It’s notoriously difficult to put a value on a private company, which Novaporte is, so any glimpse into its financial structure is welcome but I’m not sure this calculation is helpful:

Membertou’s 12.5 per cent stake in NovaPorte at $6.8 million dollars places the value of the company at $54.4 million.

George Karaphillis, dean of the Shannon School of Business at CBU, was brought in to say “that valuation is about right for what could be a billion-dollar container terminal.”

“Big projects of that size, it is reasonable that [about] five per cent of the final project is spent in trying to get the project organized initially, in trying to get it off the ground,” he said.

“Yeah, $55 million looks like it’s a reasonable amount to be able to get the project to the point where it actually can get started.”

But as Warren Buffet would be the first to tell you, you can’t always judge the value of a company by what people are willing to pay for its shares.

Membertou and Bridging were willing to accept that Novaporte is “worth” $55 million, but look at Novaporte’s “assets” as listed by Barbusci himself in the press release welcoming them as investors:

…a 99-year land lease option with the Cape Breton Regional Municipality (CBRM), long- lead time environmental approvals, Canadian Foreign Trade Zone designation, and ready access to nearby rail infrastructure connecting the site to the rest of Canada and the United States.

The Canadian Foreign Trade Zone designation is essentially meaningless and our rail line is in such parlous condition Barbusci is currently campaigning for hundreds of millions of public spending to rebuild it, so that leaves the land-lease option and the environmental approvals (about which I’m frankly skeptical, given Barbusci has yet to present anything like a detailed plan for his project).

Are we to believe Barbusci and his partner Barry Sheehy have invested millions of their own capital into Novaporte? Remember, these are the same two whose much vaunted initial $1.2 million “investment” turned out to be the value they placed on their own services ($2,500 per man per day) X the number of days they claimed to have worked on the port file (225).

Do Sheehy and Barbusci actually own 85% of nothing very much? I’m leaning toward that conclusion, especially in light of the details we now know about another project in Bridging’s portfolio: Sean McCoshen’s Alaska-Alberta Railway Development Corporation or A2A.

Compare and contrast

McCoshen and A2A are at the center of the OSC’s investigation into Bridging Finance Inc and let me be clear from the beginning: McCoshen stands accused of serious irregularities associated with his loans from BFI and I’m not suggesting there is anything similar happening with Novaporte. My point is simply that while A2A attracted publicity, received a presidential permit and was permitted by BFI to use its “assets” as security for millions of dollars in loans, the company really doesn’t seem to have had much in the way of assets at all.

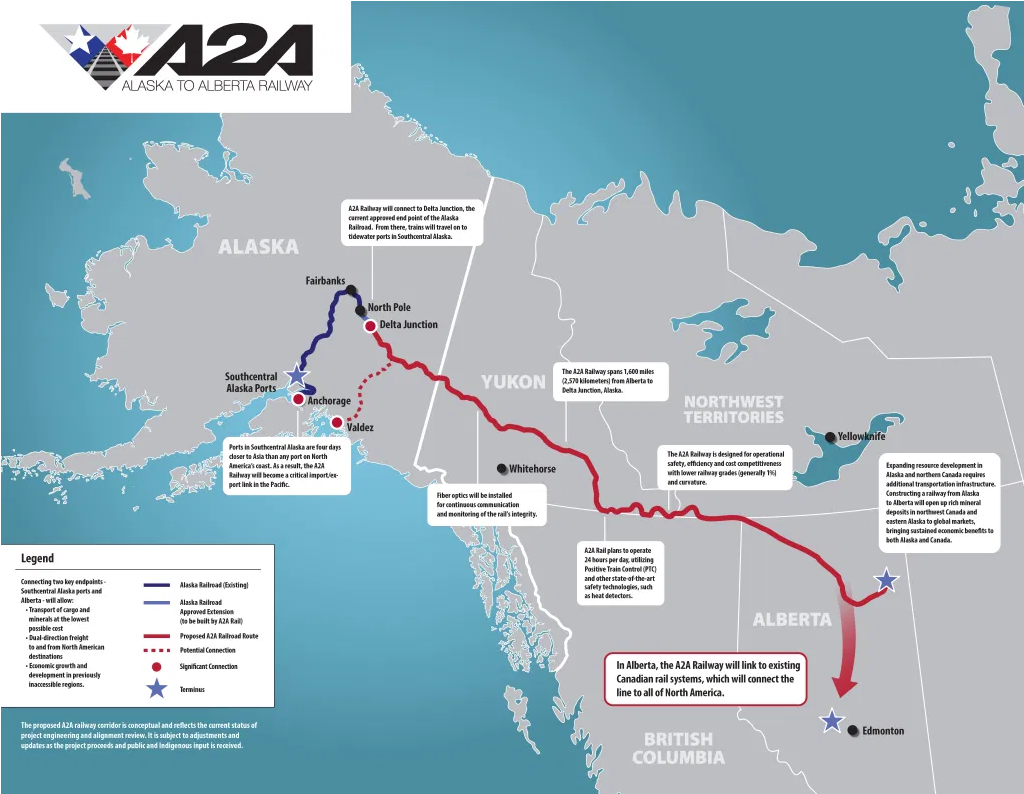

McCoshen’s ambitious plan was to construct a 2,570 km rail line from Delta Junction, Alaska to Fort McKay, Alberta and to convince the world that shipping bitumen by rail across the Canadian Arctic is a good idea. The price tag on his dream — $22 billion — makes Barbusci’s $1 billion terminal look like a bargain.

Source: A2A

McCoshen has nothing in his background to suggest he’s qualified to oversee this Herculean task. The Globe and Mail summed him up as:

…someone with a record of business failures and a vague, unverifiable résumé. One of Mr. McCoshen’s companies filed for bankruptcy, and seven years ago, he said his personal finances were “on a knife’s edge,” according to court records.

Interestingly — although not particularly germane to today’s discussion — both McCoshen and Barbusci claim ties to AECOM, the “infrastructure consulting company.” Barbusci, on the Novaporte website, goes so far as to call AECOM a “partner,” stating:

Sydney Harbour Investment Partners (SHIP) includes AECOM the world’s largest infrastructure engineering firm and all 13 First Nations communities in Nova Scotia…AECOM is also associated with the project for port engineering services.

AECOM’s connection to McCoshen’s project is more vexed — as in, is currently the subject of a lawsuit filed by proponents of a rival rail project, BC-based Seven Generations Ltd (G7G Railway), in a Manitoba court. The lawsuit, filed in June, claims that Bridging Finance, Sharpe, McCoshen and AECOM Canada Ltd “conspired” to “steal the plaintiff’s idea for the G7G Railway, misappropriate the plaintiff’s proprietary information and pursue an identical or nearly identical railway project along the route.”

Matt Vickers, CEO of G7G, told Bloomberg BNN he “hopes for a friendly resolution” to the dispute.

‘Assets’

Both the Sydney container terminal and the Alaska-Alberta railway projects apparently impressed BFI CEO and founder David Sharpe (who, by the way, is attempting to get the OSC investigation into his company “quashed”).

Sharpe had an existing relationship with McCoshen, who had brokered loans worth millions between BFI and Canadian First Nations (I don’t have time to get into this in detail, but see this Winnipeg Free Press article about Manitoba’s Peguis First Nation, a band of 10,000 people that now owes BFI $135 million.)

Between 2015 and 2021, BFI advanced $146 million in principal payments to McCoshen’s railway company, A2A, and as of 8 June 2021, according to PwC, A2A owed BFI $212,891,590, including “capitalized interest, fees, and other costs.” (See how private lenders make their money?) The loan was guaranteed by A2A, McCoshen and a handful of companies registered to McCoshen.

Both the Ontario Securities Commission (OSC) and the receiver have “significant concerns” about the A2A loan, including the fact that $82.5 million of it was diverted to yet another company under McCoshen’s control, this one with no identified “commercial relationship” to A2A. None of the allegations has yet been tested in court.

Also on 8 June 2021, the receiver demanded payment of the loan and McCoshen promptly disappeared from public sight. (PwC has been informed he is “under medical care” and unable to respond to its inquiries.) In his absence, A2A attempted to forge bravely on, along with two-other McCoshen-controlled entities it applied for creditor protection then issued a press release proposing to conduct a:

…Court supervised sale/ refinancing of the development stage of the proposed 2000-mile rail link between the existing North American rail grid, and the Alaska Railroad and Alaska tidewater port.

And now we get to the point of all this, which is that the “assets” to be sold sound very similar to those attributed to Novaporte:

…a sale of the Company’s business on a going concern basis including engineering, permits and pending permits, right–of-way agreements, marketing materials, agreements and relationships with proposed partners, First Nations and Alaska Native entities – developed for the project.

And PwC doesn’t seem convinced they’re worth $212 million:

The Bridging Receiver is particularly concerned with the value of the security held for the A2A Loan as the Railway Project is pre–construction and it is unclear whether any assets exist, other than A2A’s intangible assets, which include the Presidential Permit.

In an affidavit filed with Alberta’s insolvency court, PwC’s Graham Page said:

Although the financial situation of A2A remains unclear, based on the Bridging A2A Records, it appears that the primary assets of A2A are likely contracts or arrangements with certain parties, including: (i) agreements with those First Nations over whose land the proposed Railway Project would run; and (ii) a presidential permit granted by former president Donald Trump in September 2020 to allow the Railway Project to cross the international border between Canada and the United States (the “Presidential Permit”).

Page’s affidavit was in support of PwC’s request that the court appoint an interim receiver for A2A, arguing that allowing A2A to go bankrupt might have a detrimental effect on the value of these “assets,” including the presidential permit. The court agreed and A2A now has 45 days to come up with a plan to present to its creditors (chiefly, the Bridging receiver).

Presidential_PermitThe bottom line here is, first, that if you think Bridging’s willingness to invest in — and fund Membertou’s investment in — Novaporte is a sign of the project’s viability, you really need to read more about the A2A railway project.

And second, if you think Novaporte is worth $55 million, you should also, probably, read more about the A2A railway project.