CBRM council voted on a 5%, across-the-board — residential and commercial — property tax cut this week.

I think this chart, from the province’s Open Data portal, helps provide some perspective on this. It shows average Nova Scotia municipal residential property tax rates from 2009/10 to 2020/21. (It’s interactive, you can hover your cursor over the dots and see exact rates.)

It includes rates from the province’s three regional municipalities, plus average rates for towns and rural municipalities. What is clear is that CBRM has the highest residential property tax rates by far, although at $2.04 per $100 of assessment in 2021/22, they were actually down slightly from their peak at $2.06.

Voting record

As read by the Mayor prior to the vote, the motion, moved by District 10 Councilor Darren Bruckschwaiger and seconded by District 9 Councilor Ken Tracey, called on council to:

…reduce the tax rate for all residential and commercial accounts by 5% this year and that no services be cut [or] layoffs because of this motion.

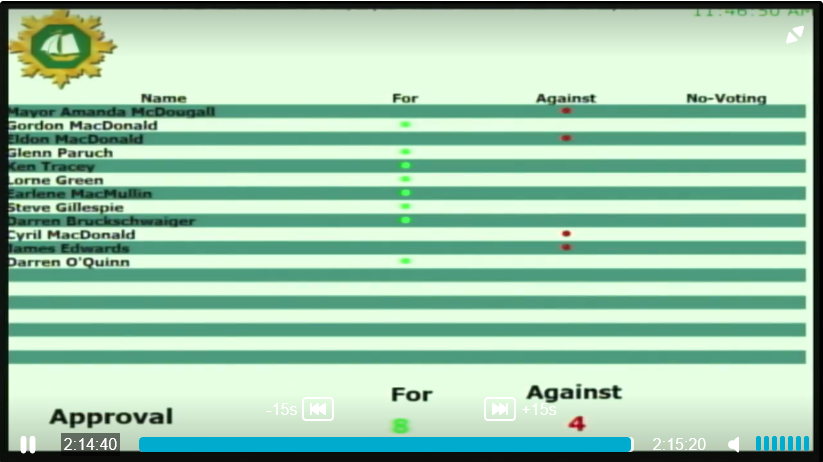

The vote looked like this:

The four votes against the cut came from Mayor Amanda McDougall, District 5 Councilor Eldon MacDonald, District 3 Councilor Cyril MacDonald and District 4 Councilor James Edwards. District 7 Councilor Steve Parsons was absent. The remaining eight councilors voted for the cut.

Why 5%?

Bruckschwaiger, who seems to be the driving force behind the tax cut, also seems to have chosen the 5% figure, and his reasoning seems to be that it will compensate for the 5.4% increase in taxable assessments this year under the provincial Capped Assessment Program (CAP).

The CAP rate is tied to consumer price inflation (CPI) in Nova Scotia and CPI has been low since 2008, when it was first linked to the CAP, but in November 2021—the date used to calculate the rate for 2022—CPI stood at 5.4%.

Source: PVSC presentation to CBRM Council, February 2022.

Both Bruckschwaiger and Deputy Mayor Earlene MacMullin, arguing for the 5% cut, referenced the belief, often expressed by critics of the CAP, that if it were lifted, property taxes could be reduced. (The argument is that the relief provided by the CAP is “phantom relief” because, faced with lowered taxable assessments, municipalities tend to raise their tax rates. If the municipality were taxing the full assessed value of accounts, it could lower its rates.)

I found Bruckschwaiger and MacMullin’s arguments on this point really confusing, though, because they seemed to be conflating the CAP rate rising with the CAP being lifted, which is not the same thing at all. Yes, people under the CAP system would have seen their taxes rise this year because of the higher CAP rate, but they would still have been better off than their uncapped neighbors. The figures provided to council by the Property Valuation Services Corporation (PVSC) in February showed total taxable residential assessed value in CBRM was $5.6. million, which dropped to $4.6 million when adjusted for the CAP. The 5% cut does nothing to address the fundamental inequality introduced by the CAP system. But maybe I’m missing something. Here’s what Bruckschwaiger actually said:

Colleagues, along with any growth we are seeing, we are now using the CAP as tax money – when I say growth that’s new builds or sales…based on staff’s numbers…I have been telling people that their rates would drop 20% if the CAP was lifted. What staff has showed us in this budget before us, we can’t make it on just yearly growth revenue, we can’t make it by that, we would either need the CAP continued or tax increases each year that is not 20% decrease in taxes if the CAP was lifted and phased out.

He seems to be implying the CAP somehow increases tax revenues when its actual effect has been the opposite. Which is why municipalities want it lifted. At another point he argued the CBRM was “picking up that revenue with the CAP” because of the 5.4% cap rate. What he didn’t say is that they’ve been missing out on revenue from the CAP since it was tied to CPI in 2008 and that those homeowners who do not fall under the CAP have always paid taxes on the full value of their assessments.

But somehow, this promise that “taxes will be reduced if the CAP is lifted” has morphed into “we’re reducing taxes because CPI rose more than it has in the past and the CBRM got a — possibly one-off — $15 million increase in its municipal capacity grant.”

Isn’t that a bit like winning $1,000 in the lottery and quitting your job?

Taxes ARE reduced

Bruckschwaiger read from a “prepared statement,” which I transcribed (for my sins, it clocked in at just under 1,500 words and should, by virtue of being “prepared” have been a lot easier to follow than it was), during which he noted the CBRM budget reflected an increase in property taxes, new monies from the deed transfer tax and an additional $15 million in the form of the doubled municipal capacity grant. In all, he said, roughly $24 million in additional funds “and still no suggestion of lowering tax rates.”

But that just isn’t true. Here’s the relevant page from the budget:

While staff didn’t envision a 5% across-the-board tax cut for everyone, they did, as you can see, incorporate a small cut for everyone, plus a small cut in the area rate for hydrant services, plus a tax reduction for low-income residents that Chief Financial Officer Jennifer Campbell said would work out to a roughly 4% to 5% for qualifying households.

Councilor Eldon MacDonald addressed this during the discussion:

The reality is that had we passed this budget the other day, I would have been voting for a tax decrease. There would have been a 1.5% decrease, I believe, cross the board, and Jennifer can correct me if I’m wrong. [She didn’t.]

How big a hole?

The CFO explained that each half-percentage-point reduction in the overall tax rate represents a loss of about $521,000. As noted above, the budget as prepared included a 1.5% tax cut, so cutting an additional 3.5% would leave a $3.6 million pothole in the budget.

For the ratepayers

A phrase used frequently by councilors supporting an immediate, 5% cut was that it was time to do something “for the ratepayers,” a concept I found utterly baffling because who are municipal roads and sidewalks and playgrounds and recreation facilities and libraries for if not the “ratepayers” or, as I prefer to think of them, “citizens?”

And can’t you do more for citizens by spending $3.6 million on collective goods than by giving each of them, individually, some small portion of that money? Back in 2020, CBU Professor Tom Urbaniak, in a Cape Breton Post column titled, “Cape Breton Regional Municipality urban decay is harming children,” wrote:

Imagine being a young person in New Aberdeen/Number 2 (or a great many other neighbourhoods). The excellent school is still open, with the SchoolsPlus program, but there is no community centre. There is no library or drop-in within walking distance. There is no bicycle path through the community. There is no place to skate or swim. There is no municipal recreation officer based in the area.

Sidewalks are uneven or non-existent, and roads are crumbling. There is still almost no action on the unsafe crosswalks in the CBRM.

This urban neighbourhood, like others in the CBRM, is what’s called a “food desert.” Although there’s still a welcoming convenience store, you have to drive somewhere else to get most groceries.

What is of more value to those children, putting money into services and infrastructure they can use or giving their parents a cut on their taxes? A cut, that, as District 8 Councilor (and former Revenue Canada employee) James Edwards explained, might not amount to much at all.

But this is starting to run as long as a CBRM council meeting so take a break and I’ll meet you at Part II: “The Tip I Left Was Higher Than What I’m Going To Save On My Taxes.”